Thought

PRI 2026: A Reset Year for Responsible Investment Reporting

The 2026 Reporting Framework from the Principles for Responsible Investment (PRI) marks a fundamental shift, not just an incremental update. For signatories, this isn’t just about learning a new template. It’s about whether your organization is genuinely ready to be assessed under a framework that is more streamlined, stricter, and less forgiving of weak foundations.

What’s changed and what it means for businesses

The 2026 framework has been significantly streamlined. Signatories will now respond to a maximum of 39 indicators, compared to as many as 257 previously. But fewer indicators do not mean lower effort or lower risk. In fact, the opposite is true.

With fewer indicators, each response carries more weight, gaps are more visible, and inconsistencies are harder to hide.

Of the 39 indicators, 30 are derived from the previous framework, meaning there is continuity. However, past practices are now being re‑tested under tighter logic and clearer assessment thresholds. Most indicators will continue to be formally assessed and scored, reinforcing accountability rather than shifting toward a purely narrative or disclosure‑based exercise.

Guidance has also been strengthened. Following extensive signatory testing earlier in 2026, PRI refined its assessment criteria and explanatory notes to improve consistency, fairness, and clarity across submissions.

Structural changes that will catch organizations off-guard

One of the most significant changes is the introduction of a unified framework for asset owners and investment managers. The 2026 framework removes the extensive, separate reporting modules previously required across different asset classes. While this may appear simpler at first glance, it introduces material implementation challenges.

In practice, it requires:

- A fully integrated view of governance, policy, and investment practices

- Clear alignment across teams that previously reported separately

- Strong internal data coherence across asset classes

For organizations that have not already addressed internal silos, this change alone can disrupt timelines and increase implementation risk.

A new baseline year

Importantly, 2026 scores will not be comparable to previous years. This updated framework establishes a new baseline, making this a positioning year rather than a benchmarking exercise.

From 2027 onwards, scores will become comparable on a like-for-like basis.

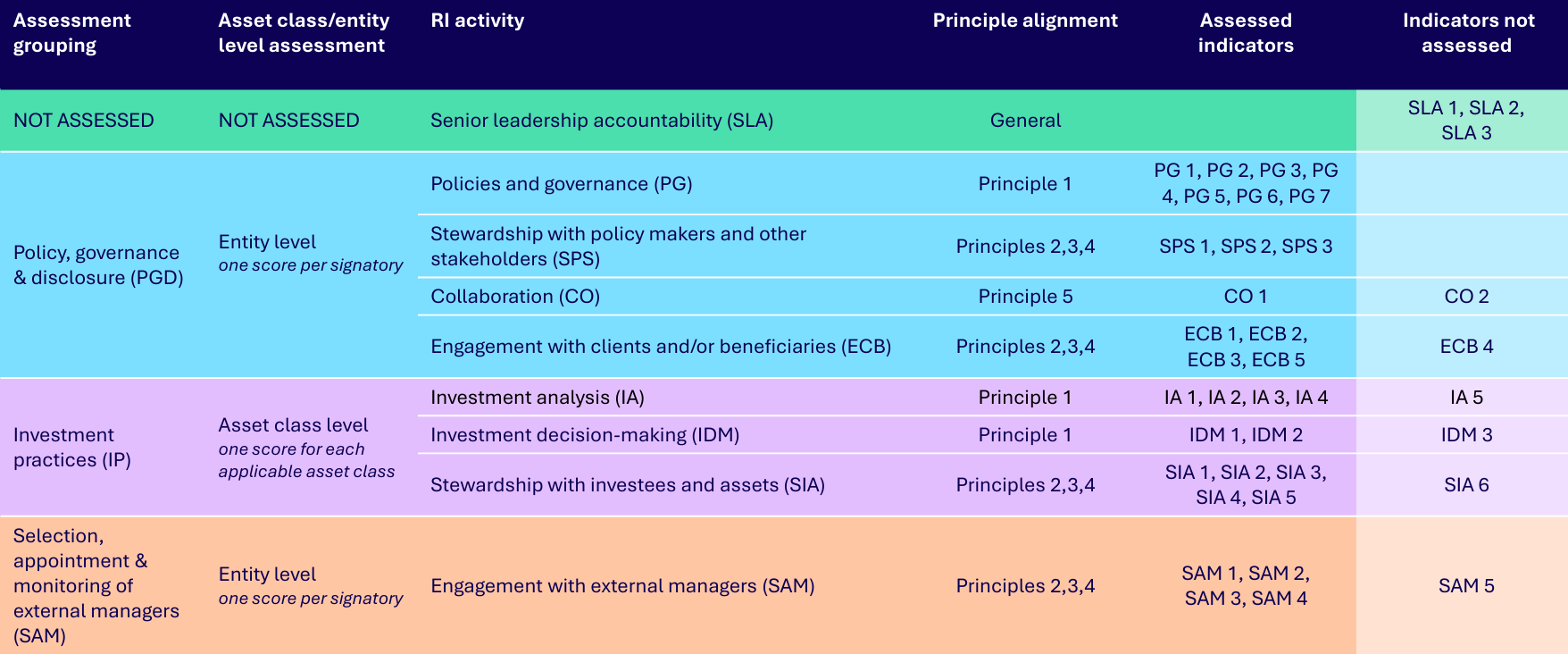

PRI 2026 Assessment Overview

The scoring structure has also evolved. Assessment and scoring are now organized into three assessment groups, bringing together related responsible investment activities:

- Policy, Governance and Disclosure (PGD) at the entity level

- Investment Practices (IP) at the asset-class level, where applicable

- Selection, Appointment and Monitoring of External Managers (SAM) at the entity level where applicable

Each group receives a group score based on the indicators reported. These group scores are then used to determine star ratings, once thresholds have been finalized after the reporting window closes and all signatory data has been analyzed. Final star rating thresholds will be shared with signatories when assessment results are released.

There will be no overall organizational level score under the 2026 framework. Where signatories report across multiple asset classes, each applicable asset class will receive its own score and star rating, while assets reported under the “Other” category will not be scored.

This revised structure changes not only how performance is assessed, but also how results should be interpreted across entities and asset classes.

Another major development is stronger alignment with global standards.

The March 2026 update introduced indicator-level mapping to ISSB, EU SFDR, and the UK Stewardship Code, supporting more streamlined and integrated reporting across regulatory frameworks.

“PRI 2026 isn’t about defending last year’s score. It’s about setting a credible starting point for future performance and accountability.” — says Nupur Sheth Patel, Senior Sustainability Consultant at EVORA.

Why delaying preparation is a serious mistake

PRI 2026 is not a light reporting year. This is not a simple update: historic responses must be reassessed, and evidence re‑validated under new logic. The risk is greatest for first‑time reporters, organizations in transition, and teams using decentralized or manual data.

Rushing this process can lock in inconsistent responses, missed scoring opportunities, and a weak baseline star rating in the first year of the new framework.

Practical reminders

- The reporting window opens 6 May and closes 29 July 2026

- Complete Organizational Profile (OP) questions early to unlock subsequent indicators and reduce last-minute pressure

- Enhanced transparency and assessment reports will be released between November and December 2026, alongside an instant report generated on submission

How EVORA can support

Navigating this transition requires both technical understanding and strategic positioning. EVORA supports clients to:

- Translate historic PRI submissions to the 2026 framework, clarifying asset-level requirements, AUM coverage, and classification impacts

- Deliver focused gap analyses and indicative scoring insights aligned to the new methodology

- Enable confident reporting through targeted workshops, improvement roadmaps, and alignment with ISSB, SFDR, and the UK Stewardship Code

PRI 2026 represents a reset, not a setback. Organizations that treat this year as an opportunity to establish a clear, credible baseline will be best positioned to demonstrate progress and leadership in responsible investment going forward.

Not sure where you stand under PRI 2026?

Get in touch for an initial gap analysis to identify the key gaps, risks, and opportunities under the new framework, so you can move forward with confidence.

Our experts also provide end-to-end PRI 2026 reporting support to help you meet the end-of-July deadline and position yourself as strongly as possible in this first year of the new assessment.